How do you store wealth?

We define an investment as the allocation of capital to a specific purpose. The four key purposes of investments in building sustainable wealth are:

Protecting Wealth

Growing Wealth

Deriving Income from Wealth

Storing Wealth

In building a plan for achieving financial independence through the accumulation of wealth, it is important that these four purposes are kept proportional to your long term needs.

Of the four purposes, the idea of storing wealth is probably the most confusing for people.

Notice first of all that we are talking about how you store wealth as opposed to where. But first, as one of my partners always reminds me, perhaps we should answer the question of “why” you would store wealth before going any further.

Most people will accumulate wealth over their lifetimes by way of employment, investing, inheritance, etc. Some people will confuse this with “savings.” However, “Savings” is simply putting aside the net gains from your past production.

If you want to ever be financially independent, you need to produce more than you consume. When you set aside the excess, that is savings.

Saving creates capital with which you can invest.

Saving creates capital with which you can invest.

However, what if you have nothing to immediately invest in? Or, let’s say that the something that you want to invest in requires a lot more capital than you currently have. In these cases, you will want to store what you have in a way that will insure that it will still have value or purchasing power in the future.

The most common store of value is money or cash.

Whether you put it in a savings account in the bank, stuff it in your mattress or bury it out in the yard, it will still be money after some number of years. In a period of inflation, however, the purchasing power of money itself will decline, undermining its function as a store of wealth. So, depending on your time frame and your immediate need, you may seek to store your wealth in other assets that at least will not lose, or would preferably increase in, value with inflation.

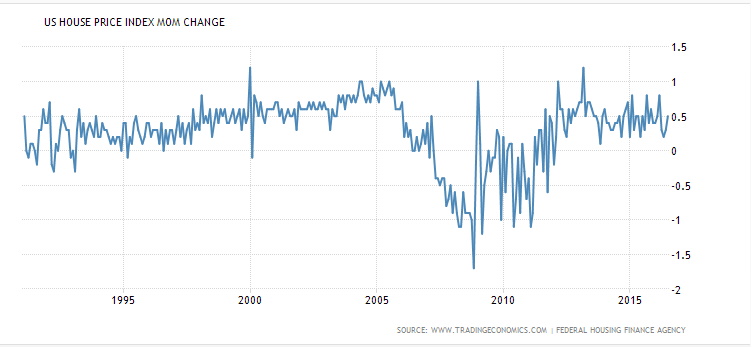

It might also make sense to store your wealth in something that could provide some utility while being used as a store of wealth. Your primary home is a prime example of such an investment for storing wealth. While many advisors will tout home ownership as a great wealth-building investment, the United States House Price Index MoM Change, which tracks the average prices of single-family houses with mortgages guaranteed by Fannie Mae and Freddie Mac in the United States, provides a more sedate view of home price appreciation since 1991.

So while you could be lucky enough to buy at the beginning of a run-up in housing prices, it is better to think conservatively and consider your home as a store of wealth that also provides some immediate utility for you and your family along with potential protection against inflation. Should an opportunity arise to make an investment to either grow or derive income from your wealth, you can easily take out a home equity loan or sell your home outright as a way to convert it back to cash.

Other examples of storing wealth include investment in precious metals, jewelry, artwork and land. Some of these assets provide you with some level of utility while others do not. But in all of these examples, you are simply choosing to store your wealth in an asset other than cash.