Second Quarter 2021 Market Review

The Recovery Continues

The second quarter continued essentially where the first quarter left off. There were few surprises that really made substantive impacts on the markets.

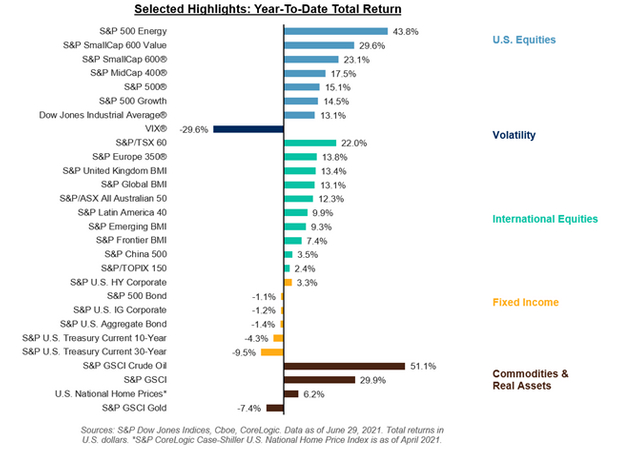

The S&P 500 climbed 8% in the second quarter, extending its five-quarter advance to an incredible 66% gain. For all the worries about tech stocks in the face of rising bond yields, the Nasdaq Composite surged 10% to take its five-quarter increase to 89%.

So far, leadership this year has come from pockets of the market that were laggards during the last decade’s rise of big tech. Using sector ETFs as a gauge, the financial sector, regional banks, value stocks and the energy sector are all up more than 20% so far this year while retail stocks have risen about 50% this year.

Small investors made the news with the rise of the meme trade. Shares of the heavily-shorted companies GameStop (GME) and AMC (AMC) have gained more than 1,000% and 2,000% this year, respectively.

Perhaps the biggest meme trade based on headlines, Bitcoin (BTC-USD) topped $60,000 before falling back to the $30,000+ range where it still sits today.

According to the Wall Street Journal, U.S. home prices surged at their fastest pace ever in April as buyers competing for a limited number of homes pushed the housing market to new records. The S&P CoreLogic Case-Shiller index rose 14.6% which is the fastest annual growth rate since the index began in 1987.

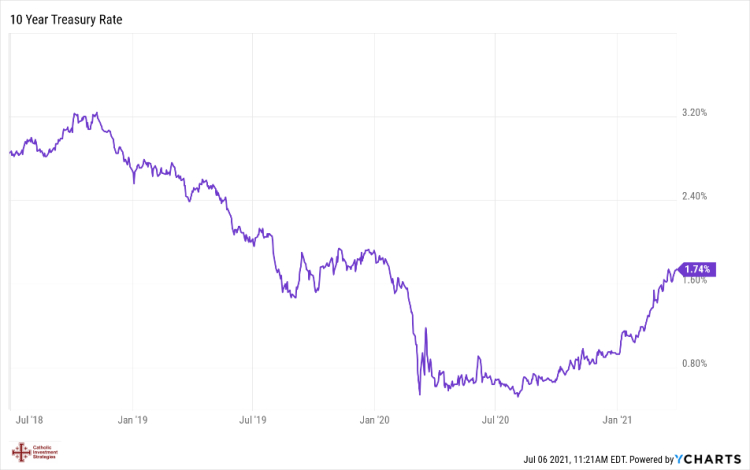

Treasury yields, which rose precipitously in the winter’s early months causing a correction in tech stocks, have dropped recently even while inflation readings hit multi-decade highs.

More recently, the White House and a group of bipartisan senators reached an agreement on an infrastructure bill, worth $1.2 trillion in spending over the next eight years.

In the last month, with the pullback of interest rates, the tech sector (XLK) and software stocks (IGV) once again outperformed the broader market.

The graph below gives a good visual of the winners and losers so far this year as of June 29th.

We would not be surprised if the market went through a correction during the second half, similar to last year when the S&P 500 Index fell 9.9% from its intraday high on September 2 to its intraday low on October 30 after a strong run up (+61.4%) from its pandemic low of late March 2020. From that point (10-30-2020), the S&P 500 has risen a very strong 32.8% so a little pullback would not be unusual.

What could cause such a pullback? There is a lot going on that can impact our investments, so here is the latest review of what is keeping us up at night.

The Economy

With the continued rise of social media combined with 24/7 news cycles and non-stop elections, we have entered what some people are calling a period of “Narrative Economics” where the prevailing narrative drives economic behavior. It doesn’t necessarily matter whether or not the narrative is true, only that the majority of participants believe it. While we think this phenomenon isn’t brand new, it seems to have gone from local to national and even international in character as technology now allows information to travel farther and wider than ever before.

As we noted in our Q1 letter, the economy was bound to recover sharply from the pandemic induced recession of 2020 which was the worst since 1946.

The economy grew at an annualized rate of 6.4% in the first quarter. Expectations are that growth accelerated to a 9% pace in the second. Demand for just about everything exploded this year. Used cars, rental cars, semiconductor chips, pilots, flight attendants, chlorine, shipping containers, and truck drivers are all in short supply and high demand. As you can see from the list, many of these items are interrelated and can cause severe short-term distortions in supply and demand pricing.

Some of these issues are already starting to abate as temporarily shuttered production facilities come back online causing supply chains to back up. But, just like a victim of a car crash doesn’t get up and start running marathons in a week, the great reopening will cycle through various fits and starts for much longer than it took to shut things down.

After a few lackluster months of hiring, the June jobs report showed non-farm payrolls grew by 850,000 last month, a signal that some of the hiring pressures within the labor market might be starting to ease.

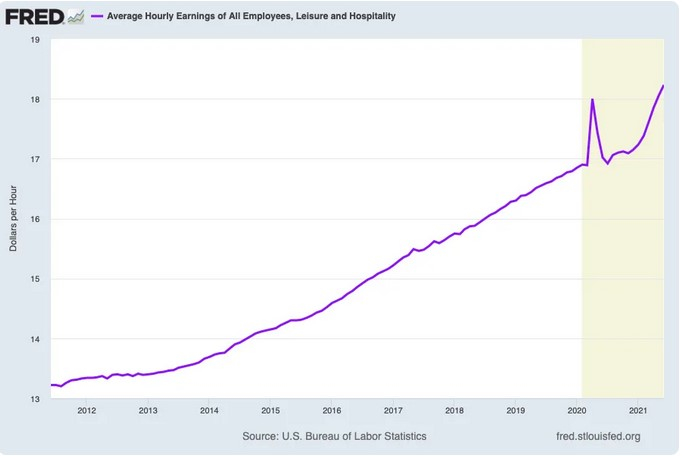

Once again, the job gains were led by the service sector where the hospitality industry continued to be the prime beneficiary of the reopening as workers returned to jobs at bars, restaurants, hotels and the like. The industry notched a gain of 343,000 new hires amid easing restrictions across the country. That total included 194,000 in bars and restaurants, but still left the sector 2.2 million employees shy of where it was in February 2020 before the pandemic began. Despite the big increase in jobs, the sector’s unemployment rate jumped to 10.9%.

That shouldn’t be too surprising as leisure and hospitality were the hardest hit businesses at the height of the pandemic.

Now, more than 154 million of 332 million Americans (46%) are fully vaccinated. The country and economy feel like they are returning to normal, and these types of businesses are dealing with pent-up demand by hiring back workers that were let go during the pandemic.

This sector has seen some of the stiffest hiring competition, and wage increases have followed as a result. In June, average hourly earnings for this sector hit a new high of $18.23, a new record for the series and a 7.1% increase over the same month last year.

Other notable employment gains came in education (+269,000) professional and business services (+72,000), and retail (+67,000).

The other services industry added 56,000 jobs, including a gain of 29,000 in personal and laundry services, a subsector that has been seen as a proxy for the resumption of normal business activity. Social assistance added 32,000, while wholesale trade contributed 21,000 to the total and mining grew by 10,000.

Manufacturing edged up 15,000 for the month, though construction lost 7,000 positions despite a sizzling housing industry where new building has been held back by supply shortages and what had been soaring lumber prices before the recent plunge.

But underneath the headline data, which also showed a slight uptick in the unemployment rate as the number of people looking for work increased, we wanted to flag a few charts outlining some of the big trends set to drive the labor market in the months ahead.

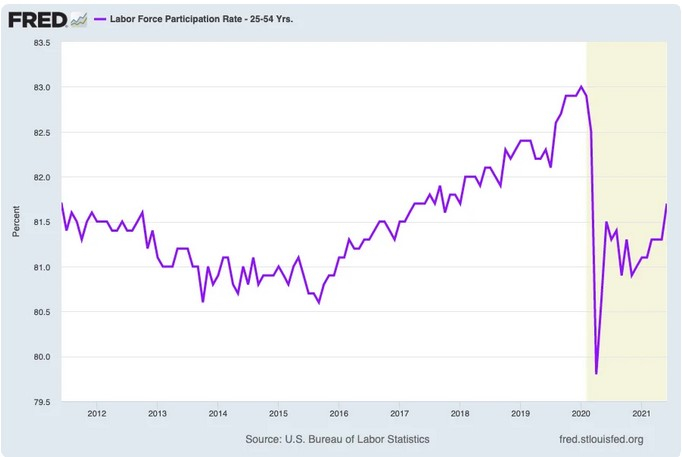

During the month, the labor force participation rate among adults 25-54 rose to 81.7%, the highest since the pandemic began and matching the level seen in January 2018.

After the 2008-2009 financial crisis, the decline in participation among prime-age workers was a major sign that the economic recovery was underserving workers and growth at-large. The rise in this rate over the second half of the 2010s was one of the most encouraging economic trends underway this century until COVID-19 disrupted the economy.

A continued rebound in participation among those enjoying the fastest career and earnings growth will be a key gauge of the health of the post-pandemic economic recovery.

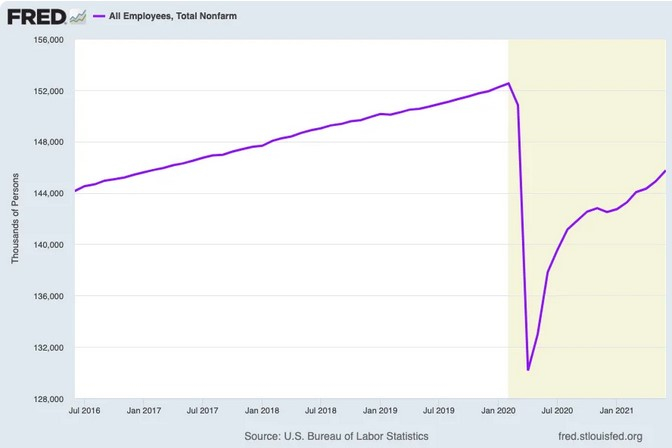

And finally, each month it is worth highlighting what remains the most discouraging labor market chart for the pandemic economy. As of June, total employment in the U.S. remained 5.7 million below February 2020 levels.

This is going to be an important statistic to watch going forward. The importance that policymakers see in this data will keep the gap between February 2020’s employment level, and any future month’s reading, near the top of conversations about the state of the labor market recovery.

Wall Street money managers and traders are trying to figure out when the Federal Reserve will begin tightening monetary policy once more.

Powell has told us employment will be the driving factor. And while it’s steadily improving, we are still far from maximum levels.

So, if we see new hires continue to steadily rise, it means the economy is inching back to pre-pandemic numbers. And that could lead to tightening monetary policy sooner than later. And while that would mean the economy is on strong footing, it could also remove a key pillar of support for the current market rally.

The prevailing narrative today is that we are recovering and will return to the pre-Covid economy soon.

The stock market is pricing in that more pleasant future. Any shift from that narrative could cause a reversal in the markets which, as we have discussed before, will now get amplified by the algo-traders rushing to beat everyone to the exit.

Treasury yields signal investors’ waning economic exuberance – WSJ. The recent drop in U.S. Treasury yields reveals some investors’ doubts about how strong the economy will be in the coming years, even as inflation pushes to its highest level in more than a decade.

The other risk, which we will discuss below, is that the recovery happens “too fast” which could impact interest rates and bring a halt to the rally.

The Fed

If you recall, the growth-heavy Nasdaq Composite Index almost fully corrected in Q1and only managed a small gain due to a sharp rise in interest rates. Long rates exploded higher throughout Q1, with the yield on 10-year US Treasury bonds rising 15bps (Jan), 34bps (Feb), and 34bps (March).

US 10 Year Treasury Rates through March 21

This sharp reaction by the NASDAQ 100 only serves to strengthen the narrative that Wall Street is addicted to low interest rates and the Fed is a prime driver of near-term stock prices.

The Fed’s primary goals are to promote maximum employment, stable prices, and manage long-term interest rates. The Fed also helped to create stability in the financial system at the height of the pandemic last year. An April 13th, 2020, post at CNBC.com details the almost $6 trillion in stimulus the Fed provided to the economy in addition to the $2 trillion from the Government’s first rescue package.

Whether we agree that stimulus at the onset of the coronavirus pandemic was a good idea or not, it did what it set out to do.

The Fed orchestrated the stability of the financial system and staved off economic collapse. Chairman Jerome Powell has even said the Fed’s worst-case scenarios never came close to playing out. But now that the crisis has been averted, the emergency policies will eventually need to be reversed.

If economic growth this year can reach 8% as some Wall Street economists have suggested, it will mean we are recovering to pre-pandemic levels.

That would be a signal it is time for the central bank to back away from easy-money policies. That would mean taking steps like diminishing bond purchases before it begins to actively raise interest rates. In fact, several Fed members have begun hinting that the time may be right to get started.

Fed’s Waller says 2022 rate hike possible, wants MBS taper first – Reuters. A “very optimistic” Federal Reserve Governor Christopher Waller on Tuesday said the U.S. central bank may need to start dialing down its massive asset purchase program as soon as this year to allow the option of raising interest rates by late next year.

Kaplan hopes Fed will begin bond taper soon – WSJ . Federal Reserve Bank of Dallas leader Robert Kaplan reiterated his view that it will soon be time for the U.S. central bank to slow the pace of its $120 billion a month in bond buying stimulus, a process he expects to go smoothly.

Based on the current data, the Fed could begin to reduce bond purchases by the end of this year with an eye to start slowly raising interest rates in late 2022 or early 2023.

While it may not be what Wall Street wants to hear, it is the practical course to take. Maintaining current easy money policies could have bad economic implications down the road with serious inflation and a declining dollar.

Declining stimulus, though, could have negative implications for the S&P 500 and NASDAQ Composite Index next year. So, they are weighing short term versus long term risks. Guess which usually wins.

Tax Policies

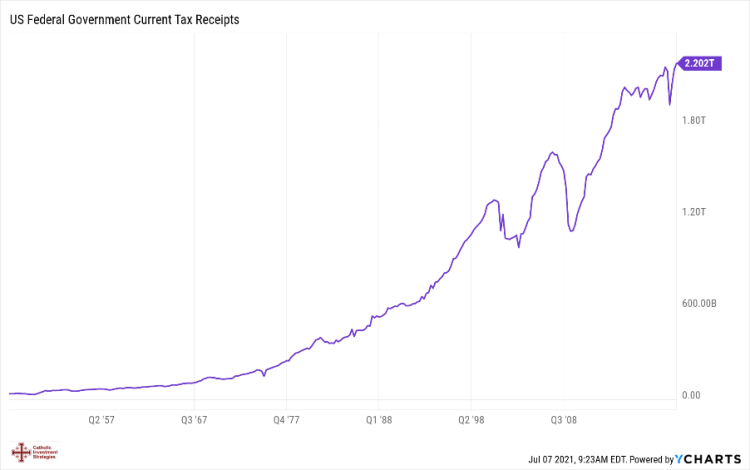

As of the first quarter, US Federal Tax receipts topped $2.2 Trillion for the first time, beating the previous high point from the fourth quarter of 2019 (see chart below). Yet, despite record setting tax receipts, the chorus of those calling for new taxes seems to be endless.

In a May interview in The Atlantic , former Fed Chairperson and now Treasury Secretary Janet Yellen claimed that an approximate $7 trillion in taxes are going uncollected by the federal government. It is being made clear that raising taxes will be a priority of the current administration.

As we pointed out last quarter:

“According to MMT, you do not need taxes to pay for government spending but instead:

1. To force citizens to accept government currency by forcing them to pay taxes in the same currency.

2. To reduce any economic imbalances by using the progressive tax code to address income inequality by taxing the rich and redistributing it to lower income individuals.

3. To fight inflation, instead of raising interest rates, the government would cool the economy down with a large tax hike.”

With government stimulus to date exceeding $6 trillion, a bipartisan $1.2 trillion infrastructure bill on the table and a promise to use budget reconciliation to push through additional spending, we can certainly argue that Washington D.C. has embraced MMT in spirit if not in name.

Some of these proposals are for actual tax increases like returning the top rate to 39.6% and the top corporate tax rate to 28%.

Many other proposals are categorized as “fixes” to the tax code to eliminate “loopholes” in the system. Apparently, denizens of Washington think the average voter can be made to believe “someone else” will foot the bill.

Again, these are just proposals, so we won’t get into them here.

The current list is posted at whitehouse.gov. Our focus is how any new tax impacts our investing strategies. Any tax that reduces net incomes or increases costs can certainly negatively impact domestic economic growth which, in turn, could negatively impact stock prices.

Any taxes which impact estate planning or real estate investments can result in short-term volatility as people and businesses scramble to adjust portfolio structures to avoid additional taxes. The proposed limits on 1031 exchanges, taxing capital gains as ordinary income, and elimination of the stepped-up basis for inherited assets are examples of this.

We will continue to watch developments and keep you informed as to any impacts on our strategies.

Geopolitics

In recent articles and interviews, Michael Pillsbury from the Hudson Institute and the author of “Hundred Year Marathon” sees a stronger alliance growing between China, Russia and Iran.

Pillsbury said that though a “global world order” was set up by the United States in 1945, the Russians and Chinese want to challenge that world order.

“This is a strange challenge coming from these two powers. And when they bring in Iran, I mean, Iran is the source of their oil and gas. It’s got a lot of money to buy weapons. They see it as the main way to tie down the Americans in the Middle East.”

Indeed, the recent election of a new President in Iran only strengthens this notion.

An article in Asian Times, published shortly after the first press conference of newly elected President Ebrahim Raisi, noted that Iran’s path ahead is unmistakable. That path is centered on the “Look East” strategy, which means closer cooperation with China and Russia. Iran will be a key node of Eurasian integration (or, according to the Russian vision, the Greater Eurasia Partnership).

“In terms of Big Power politics, Iran’s “Look East” policy was devised by Khamenei, who fully vetted the Iran-China comprehensive strategic partnership worth $400 billion, which is directly linked to the Belt and Road Initiative. He also supports Iran joining the Russia-led Eurasia Economic Union (EAEU).

China will be investing in Iranian banking, telecoms, ports, railways, public health, and information technology – not to mention striking bilateral deals in weapons development and intelligence sharing.

On the Russian front, the impetus will come from the development of the International North-South Transportation Corridor (INSTC), which directly competes with an east-to-west overland corridor encompassing Iran, Iraq, Syria and Lebanon.”

Are these developments just a natural outgrowth of developing nations looking to diversify through trade and economic expansion or are they seeking economic and military dominance? We don’t know. What matters here is how the US reacts to developments around the world and how it impacts us at home.

We have already seen a much bolder stance coming from China and recently Russia in face-to-face meetings with administration officials. And the restarted nuclear talks with Iran are either making good progress or falling apart depending on which news source you read.

In many ways, this feels very much like a reversal of the late 1980’s when the US was able to collapse the weakened USSR by forcing them to focus on geopolitics and military power instead of building a stronger economy.

Back then, the US did very little trade with Russia which, because of their closed economy, was eventually unable to fund their political and military ambitions.

However, China is a different story. It was long believed by our government that opening trade with China would result in a kinder, gentler, and more “democratic” Chinese government. Today, the US is still China’s largest trading partner making up 17.5% of China’s exports, including, as we learned during the lockdowns, goods and materials critical to many of our industries. So, thanks to us along with much of Western Europe, China is in a much stronger position for an economic battle.

Inflation

Here’s an interesting thought exercise for all of our clients who are homeowners. If you have owned your home for the last ten years and it is appraised for sale at a higher price than you purchased it, is it actually higher in value, or is it simply that a dollar won’t buy as much house as it did ten years ago?

After nearly a decade, a day does not go by now without at least one article about inflation hitting our screens.

Inflation eats at surging U.S. pay with Biden plans at stake – Bloomberg. Americans are enjoying outsized pay boosts this year from desperate employers, but the raises are failing to keep pace with surging prices for everyday goods.

There is no question that we have seen significant price increases over the last six months. Lumber had become a hot commodity, with home builders like Wisconsin’s Dave Belman posting pictures of what a difference a year can make.

Chalk it up to the law of supply and demand. Demand for lumber from single-family housing construction was outpacing existing lumber capacity and driving gains in lumber prices. Meanwhile, the supply of lumber was limited due to the shutdown of the economy. But as many states begin to resume economic activity, we are seeing the price of lumber recede from the most recent highs.

We are seeing similar behavior in other commodities as more production comes online and pipelines begin to fill up.

The big exception is in the energy sector where everything continues to climb:

But again, this price action can be explained by supply and demand. In the first six months of a new administration, daily U.S. oil production has fallen by 1.715 million barrels from a year ago. One of the first acts of the new administration was to cancel the Keystone XL Pipeline project, which would have brought crude oil down from the oil sands of Canada to the Gulf of Mexico. The administration also ended drilling licenses in the Arctic National Wildlife Reserve and stopped new drilling on federal lands, thereby making it harder to drill, transport, and produce oil.

As a result, energy futures, which are forward-looking, are reflecting a sentiment that the supply of oil will not be able to keep up with demand. Therefore, they indicate that oil will be even more expensive in the days to come.

Price increases are the consequence of inflation. They are not inflation itself.

Instead, price increases may represent a temporary imbalance between supply and demand as we pointed out above.

In classical economic terms, inflation occurs when the real purchasing power of a currency declines. Your home price, as noted above, has most likely risen in dollar terms. The utility of the home has not changed, it just takes more dollars to buy it. But we’re certainly happy with the price appreciation, as it makes us feel “richer” even though a quick search on Zillow would tell you that many other people are experiencing the same “gains.”

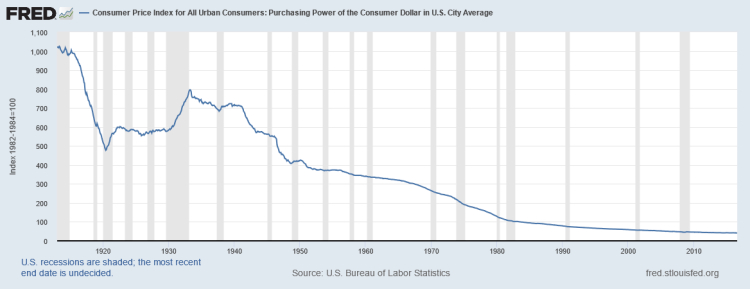

The purchasing power of a “consumer dollar” in an average US city.

The pandemic has led authorities to create an enormous amount of money.

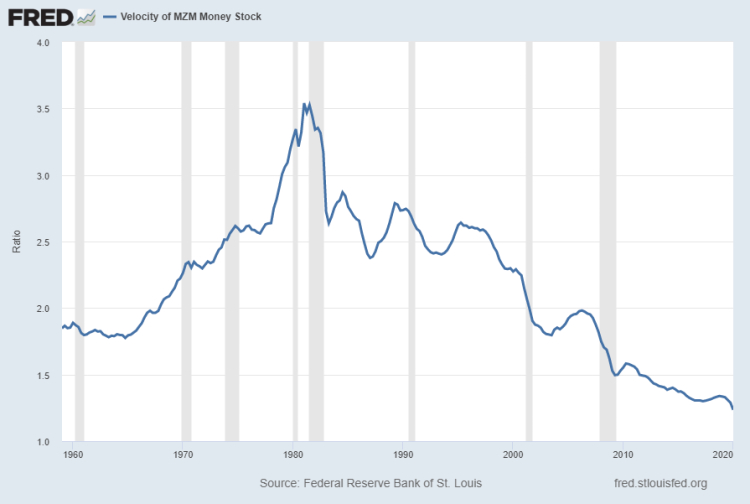

However, for all that money printing to have an inflationary effect, it requires the velocity (or turnover) of that money to increase. Meaning that once the money gets printed, it needs to be spent so that it flows through the economy. For quite a while, including right now, that hasn’t been happening.

The pandemic and ongoing lockdowns struck fear over their health into the hearts of many Americans. They also created widespread financial fear in the hearts of many people who, instead of spending the stimulus money they received, either increased their emergency reserves or paid down debt. As a result, the money was neither spent nor lent. While we applaud increasing reserves and paying down debt, neither action does anything to “inflate” the economy as all that money creation was intended to.

Make no mistake, the Federal Reserve and the U.S. government want inflation.

Why? Because with the U.S debt-to-GDP level hovering near a record 130%, they need it.

There are only three ways to reduce government debt, raising taxes, reducing spending, or erasing it through inflation. While the administration appears anxious to raise taxes, they know that it’s impossible to raise taxes enough to pay off the debt without bringing the economy to a halt, much the way the lockdowns did. As for cutting spending, please don’t get us started.

Therefore, inflation is really their only viable option. Inflation reduces the value of cash; causing the value of the debt as a whole to decline. As inflation increases the Gross Domestic Product (GDP), the debt shrinks in value and becomes easier to pay. In 1946, the debt to GDP ratio was 108.6%. Inflation over the next decade reduced this ratio by about 40%.

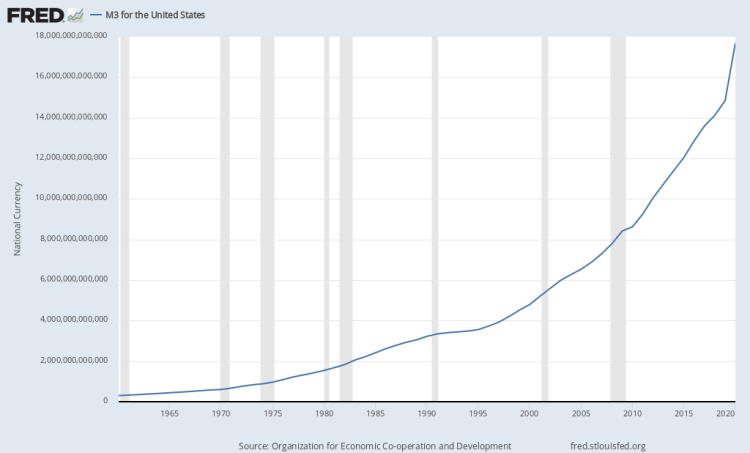

Looking once again at the M3 chart above, we can see that since 9/11, the Fed has been trying to create inflation to stay ahead of the government’s deficit spending.

Unfortunately, as is the case when most economic theories are actualized, people are not behaving as the theories expected. Nonetheless, we do not expect the government to give up. Consequently, inflation will eventually raise its ugly head. When it does, we will be ready.

One thing to keep in mind, as Marc Lichtenfeld, author of “Get Rich with Dividends” and “You Don’t Have to Drive an Uber in Retirement” recently posted:

“… along with hard assets such as oil, natural resources, gold, silver and real estate, by investing in the right dividend stocks, we can keep up with inflation and prepare for retirement without the worry of losing it all to market volatility.

For starters, most dividend-payers are mature, stable companies that are often leaders in their field. And second, in many cases, their dividend payments handily beat the rate of inflation.” When we buy shares in stable, dividend-paying companies, not only are we investing in a stock that’s delivering steady share price appreciation…we’re also getting additional income in the form of regular dividend payments.

This not only helps us prepare for retirement but face the ever-present danger of inflation, as well.”

Therefore, when we consider periods of higher inflation, we are not really talking about making large, structural changes to our strategies, just ensuring that the mix is appropriate for the economic environment.

Are you an investor or a speculator?

We know that we can sound like a broken record on this topic, but we also know that many of you are constantly bombarded with news and emails about buying high-flying tech stocks, heavily shorted meme stocks like GameStop (GME) and AMC Entertainment (AMC), or crypto currencies to capture exceptional gains. The fear of missing out (FOMO) is a powerful emotion.

Good, stable companies that pay dividends at an increasing rate are boring and rarely make the news, which, as investors (not traders or speculators), is what we want.

Which brings us to a final point on returns. We are all human, and it is human nature to try to find something that measures success. We push our kids to get straight A’s thinking that is a measure of their intellectual growth. We track our handicap in golf and our bowling and batting averages to measure our ongoing improvement. Just like you, we feel good when we look at our investment statements and see more money in the account than the period before.

But our goal shouldn’t be to have beaten the market every time we look at our account statement.

Rather, we should be looking to build a portfolio of businesses that will stand the test of time due to the nature of the business and industry. And by test of time, we’re talking about years, not the next month or 3 months or even 12 months. On top of that, we should be attempting to become owners of those businesses when the price is attractive. That is how we believe a portfolio should be built and assessed.

Speculators, on the other hand, aren’t thinking about the long term or the value of the business all that much. Primarily, they are making decisions based on what they believe other speculators might be willing to pay for the security in the not-too-distant future.

We end up with two different sets of viewpoints operating in the market. The investors will take a pass on the speculative companies that are trading on narratives that can’t be effectively analyzed. For their part, the speculators avoid the “boring” companies (often with solid balance sheets and high profits) that lack an exciting hyper-growth story. The result is two very different market segments with very different valuations existing, side by side, in the same market.

In any given month, quarter, year, or even decade, these two groups are competing for supremacy. When the speculators are in the driver’s seat, the stock price of many companies that do not fit our criteria will raise the market to ridiculous levels. During those times we will likely underperform the averages.

Companies, too, can take advantage of a frothy market. As noted in a recent post by Bloomberg (Investors Will Buy Anything Now – Bloomberg ), since the end of March alone, nearly 100 unprofitable companies have sold more of their shares on the open market. Every share sold raises funds for the company but also dilutes the ownership stake of the existing shareholders.

Over the past 12 months, some 750 unprofitable firms have sold shares. They are diluting their current owners’ stakes while valuations are high, investors are flush with cash, and speculation is rampant.

If we need to buy shares in companies like these to beat or even just compete with the broad market, we will gladly accept our lower returns.

As we have mentioned in conversations, if you really have an itch for speculation, we strongly suggest that you open a small trading account with which you can apply some of the ideas you are bombarded with each day. We are always happy to discuss such strategies with you and provide educational resources to help you make it a successful pastime. However, we will also remind you that this is not investing, and that success can be fleeting.

In closing

Finally, for those of you actively logging into your Summit Client Portals you will see the enhancements that have been made in hope that the information is more transparent and informative. The portal also gives you access to your quarterly reports and client letters as soon as they are posted instead of waiting for the mail to arrive.

We have now launched a mobile version of the portal so that you can access it on your Apple or Android phone. We have had several clients begin using the app and, so far, the feedback has been positive. If you would like to have this ability, please contact us and we will get it set up for you.

We leave with you with our best wishes for a happy and pleasant summer.