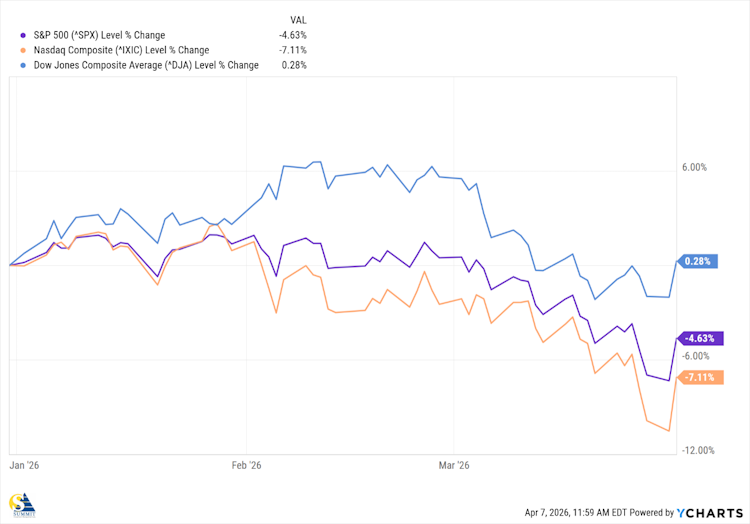

The major indices limped into the end of the quarter with the Dow Industrials barely eking out a gain, while the tech-heavy Nasdaq and the tech-weighted S&P 500 finished below where they started.

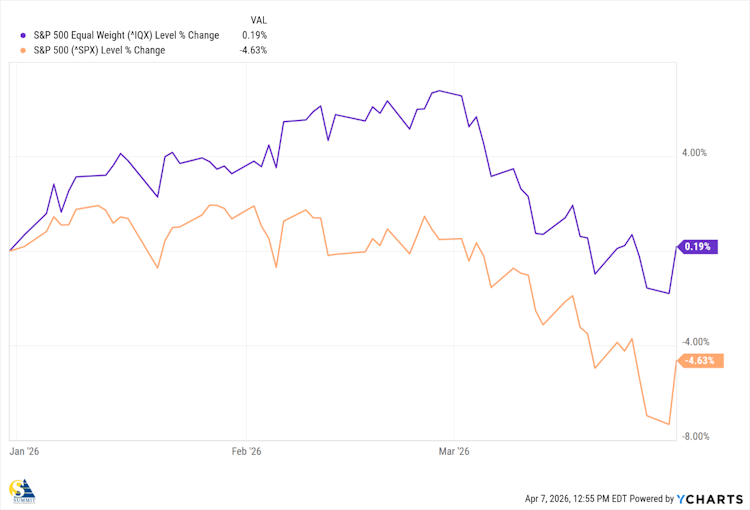

Demonstrating the impact of tech stocks on the S&P 500, the index’s equal-weighted version comfortably outperformed its cap-weighted version, where the Mag-7 make up nearly 30% of the index.

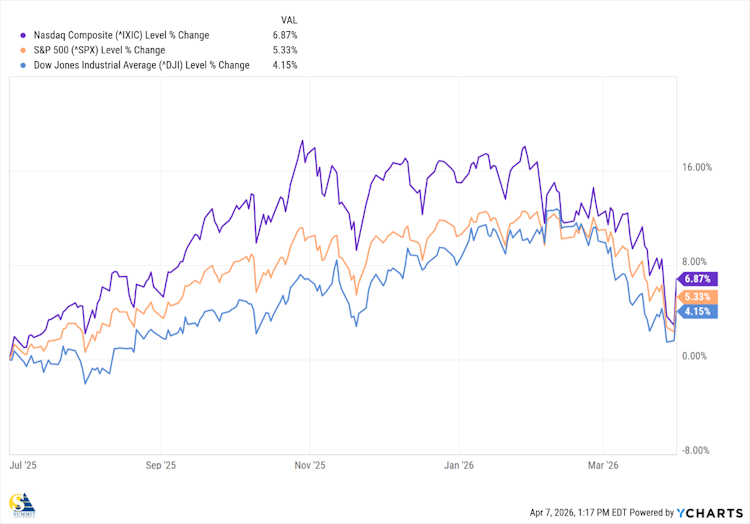

While most of the downturn happened since the start of the Iran conflict, tremors began to appear in the fourth quarter of 2025, especially on Nasdaq.

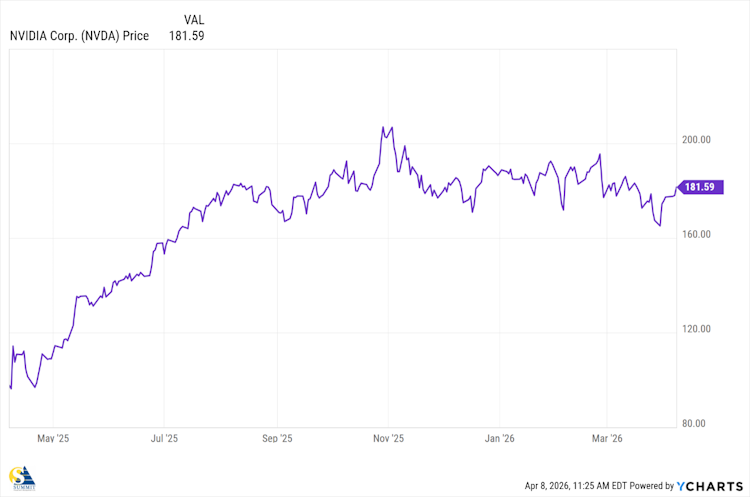

It started with talk of an AI bubble in November. We addressed the arguments, both pro and con, regarding the AI bubble in our Q3 2025 Letter and, in our Q4 2025 Letter, suggested that we would start to see a clear separation between AI winners and losers this year. However, even clear AI dominators like Nvidia Corp, showed signs of stress as the share price has been relatively flat since November.

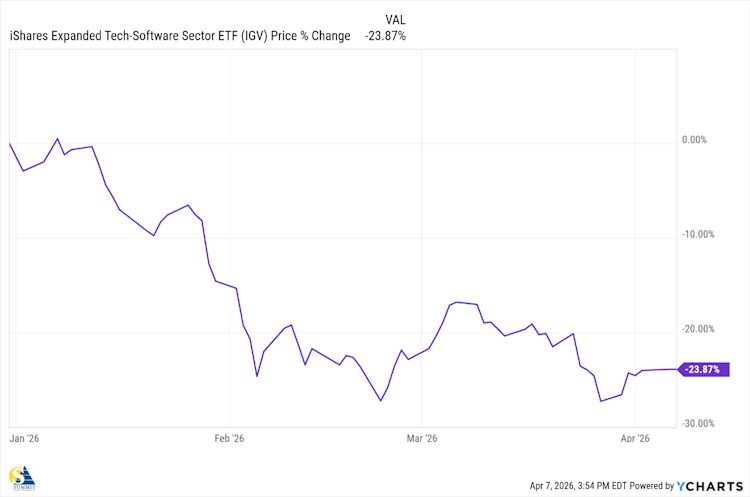

Then, starting in January, we saw another meme emerge: “AI will eat the world!” It started with software providers. Traders began selling software stocks in a frenzy after the company, Anthropic, announced new updates to its enterprise AI suite of tools that allow AI agents to independently execute complex, multi-step professional workflows—such as reviewing legal contracts, drafting documents, and automating data analysis—rather than just acting as simple chatbots that we are familiar with.

Investors panicked because the update signaled that AI could directly replace recurring software licenses and headcount-based service models, leading to a “SaaSpocalypse”. SaaS stands for Software as a Service and was the next big thing, not too many years ago, as part of the smart home movement.

The iShares Expanded Tech-Software Sector ETF (IGV) dropped 24% within weeks of the announcement and has yet to recover.

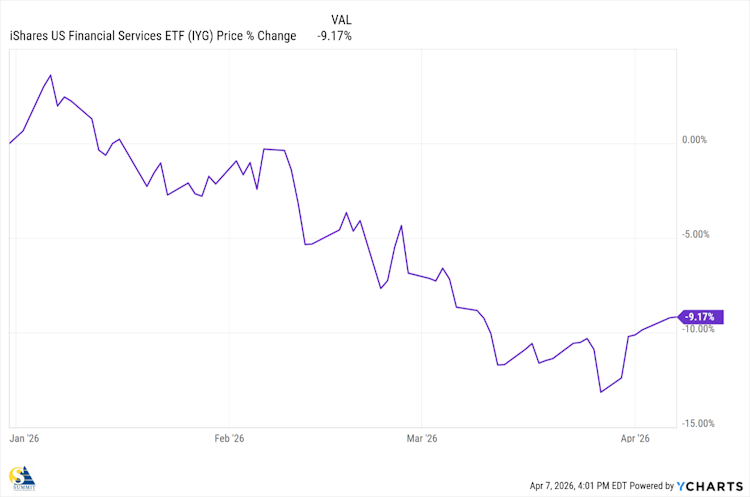

Not long after that, we started hearing of fears that AI would make banks and financial institutions obsolete, leading to a drop in financial stocks. iShares US Financial Services ETF (IYG) fell nearly 8% in a matter of weeks.

We note that these two investment themes, the AI Bubble and AI is Taking Over, seem to be contradictory at first blush. However, just as with the internet or the “Dot-com” Bubble, both themes can be valid simultaneously. While the 77% drop of the Nasdaq index wiped out many worthless companies, it also created a tremendous buying opportunity for many companies that have shaped our economy, including Apple, Google (now Alphabet), and Amazon.

AI is another technological leap forward, and the winners will also have a tremendous impact on our economy. But progress never advances in a straight line and we should expect to see distortions and displacements along the way that will need to be managed with patience and objectivity.

The market action has also rattled the private credit markets. It is said that private credit portfolios hold many loans to start-up software firms, so if these companies are driven out of business by AI, they won’t be able to repay those loans. Nervous investors in space started trying to get their money back. In the first quarter, they asked to withdraw nearly $14 billion from a major group of private credit funds.

The problem is that private credit portfolios aren’t as liquid as stock portfolios. There are limits to how much money they can give back to investors, and as a result, most funds started capping withdrawals, which is the last thing you want to see if you’re worried about your investments.

As a result, some of the major publicly traded private credit (and private equity) firms have incurred stock losses since then. Ares Management (ARES), Apollo Global Management (APO), and Blue Owl Capital (OWL) are among the largest private credit managers, and their stocks have fallen sharply recently.

We do not think this is a repeat of the 2008 mortgage crisis; however, we will stay on top of the situation and take defensive action if circumstances warrant. But it is also a lesson about chasing returns without a full understanding of the underlying market.

We have no doubt that the short sellers who drive much of this downward pressure would have gone down the list of health care, communication services, and information technology if not for the start of the Iran conflict.

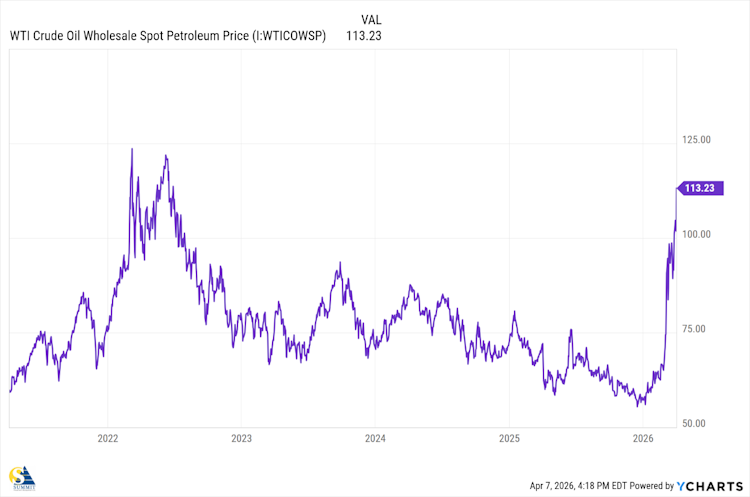

The conflict started on February 28th and, as of this writing, still continues. Oil prices, as measured by West Texas Intermediate (WTI), have continued to climb with each passing week and are now approaching levels last seen in 2022 at the onset of the Russia-Ukraine conflict.

We have no idea how or when the Iranian conflict will end, but we do have data on market behavior during military conflicts.

The Market & War

Historical evidence shows that U.S. stocks are often volatile at the onset of war or geopolitical conflict but tend to stabilize and perform well once uncertainty is resolved.

This is because markets generally react not to the conflict itself, but to changes in expectations—duration, economic disruption, inflation, and policy response. When a conflict begins, the large, index-moving investors often de‑risk, producing short‑term drawdowns. Once the scope becomes clearer, equity markets typically refocus on fundamentals such as earnings growth, fiscal stimulus, and productivity.

This pattern is visible as far back as World War II, when U.S. equities rose meaningfully despite global devastation, supported by industrial expansion and government spending. Similar behavior occurred during the Korean War and the Vietnam War, in which markets experienced interim volatility but ultimately advanced over the life of the conflict. Even during smaller, more acute events such as the 1990–1991 Persian Gulf War, stocks declined sharply ahead of combat operations but rebounded quickly once military clarity emerged, with the S&P 500 posting strong gains in the year following the invasion.

The chart below is a schematic, long‑term visualization of U.S. equity market behavior (indexed growth) with major conflicts annotated:

While no two periods are identical—and inflation, interest rates, and valuations matter greatly—the consistent lesson is that short‑term geopolitical shocks have not prevented long‑term equity growth.

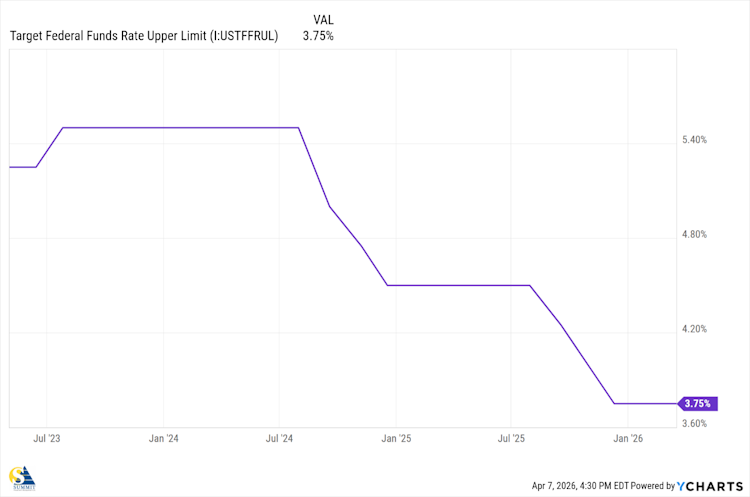

We believe investors are more worried about interest rates, as the spike in oil prices will undoubtedly lead to higher prices, leading the Federal Reserve to maintain rates where they are, or even start increasing them if oil prices remain elevated.

Earnings

On the fundamentals side of investing, the S&P reported 14% earnings growth in Q4 2025, marking the 5th straight quarter of double-digit earnings growth, according to Factset.com.

The Information Technology sector reported the highest earnings growth among the 11 S&P 500 sectors, at 33%.

73% of the companies reported earnings that exceeded analyst estimates, which is below the 5-year average of 75%, 51 companies issued positive EPS guidance for Q4, and 59 have issued positive guidance for Q1 2026, which is the highest number in 5 Years, and Industry analysts in aggregate predict the S&P 500 will see a price increase of 28.9% over the next twelve months. This again is well above the historical average.

This bodes well for at least having a “floor” where valuations present buying opportunities in financially strong companies.

As we mentioned in the Q4 letter, volatility is going to be around for a while as the market reprices every earnings, economic, and geopolitical report. Additionally, 2026 is a midterm election year, which has tended to be the worst year of the four-year Presidential cycle. Looking at the midterm years of this century, 2022, 2018, 2014, 2010, 2006, 2002, the S&P 500 index was down an average of 2%. Going back to the 1950’s, midterm years have historically been the worst, with an average intra-year drawdown of 18% from peak to bottom, according to PinPoint Macro Analytics.

For investors with clear objectives and defined time horizons, volatility can be mitigated in the short term and present buying opportunities for the long term. This is why we spend so much time on suitability and modeling your personal finances, so the investments are allocated to align with your personal needs and timing. We don’t try to predict what the markets will do next week, next month, or next year; we prefer to position our investments so that our plans are not disrupted by whatever happens.

We thank you for putting up with our surveys and questionnaires; the information helps us uphold our fiduciary duty to always put your individual needs first.

As always, if you’d like to discuss anything in the updates or the quarterly reports, please contact us at your convenience, and we’ll always be happy to connect with you.